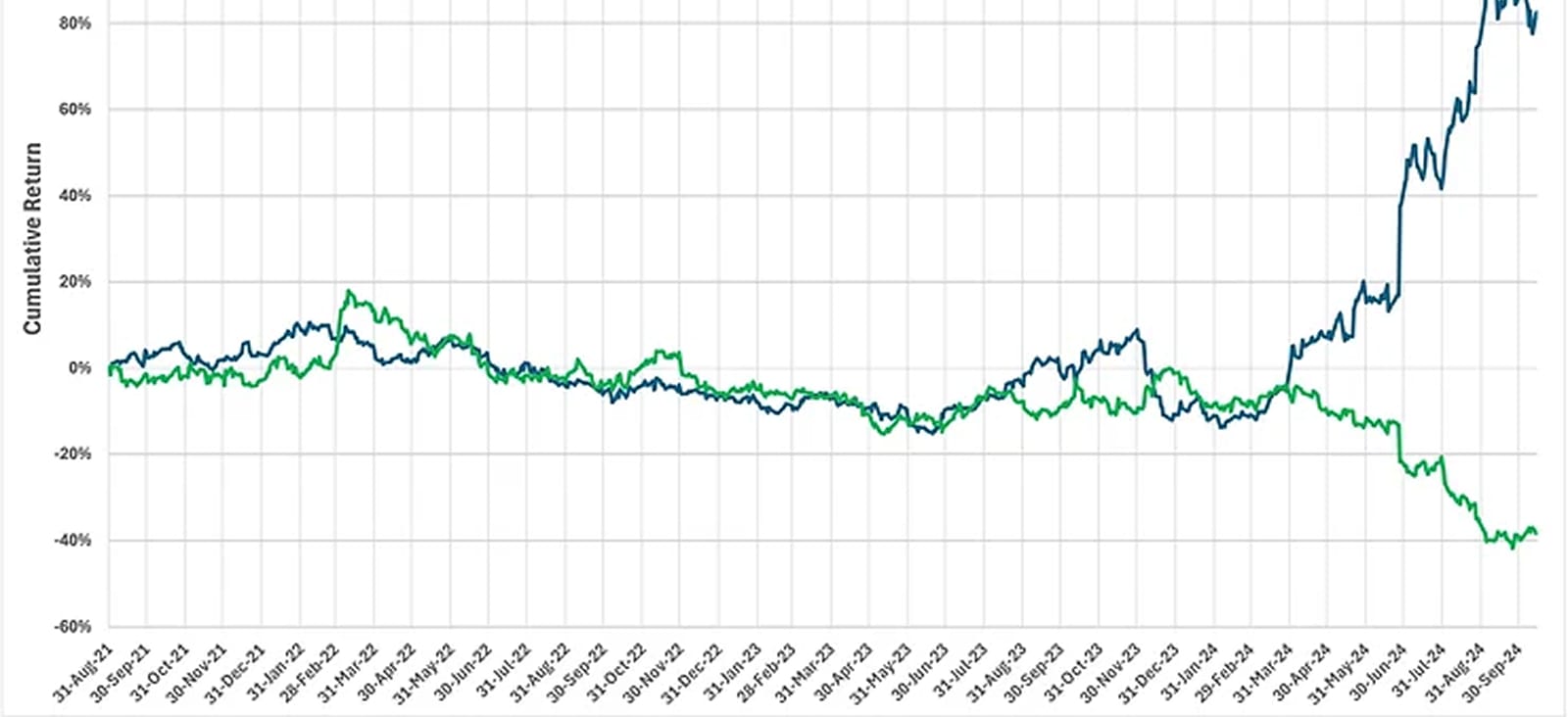

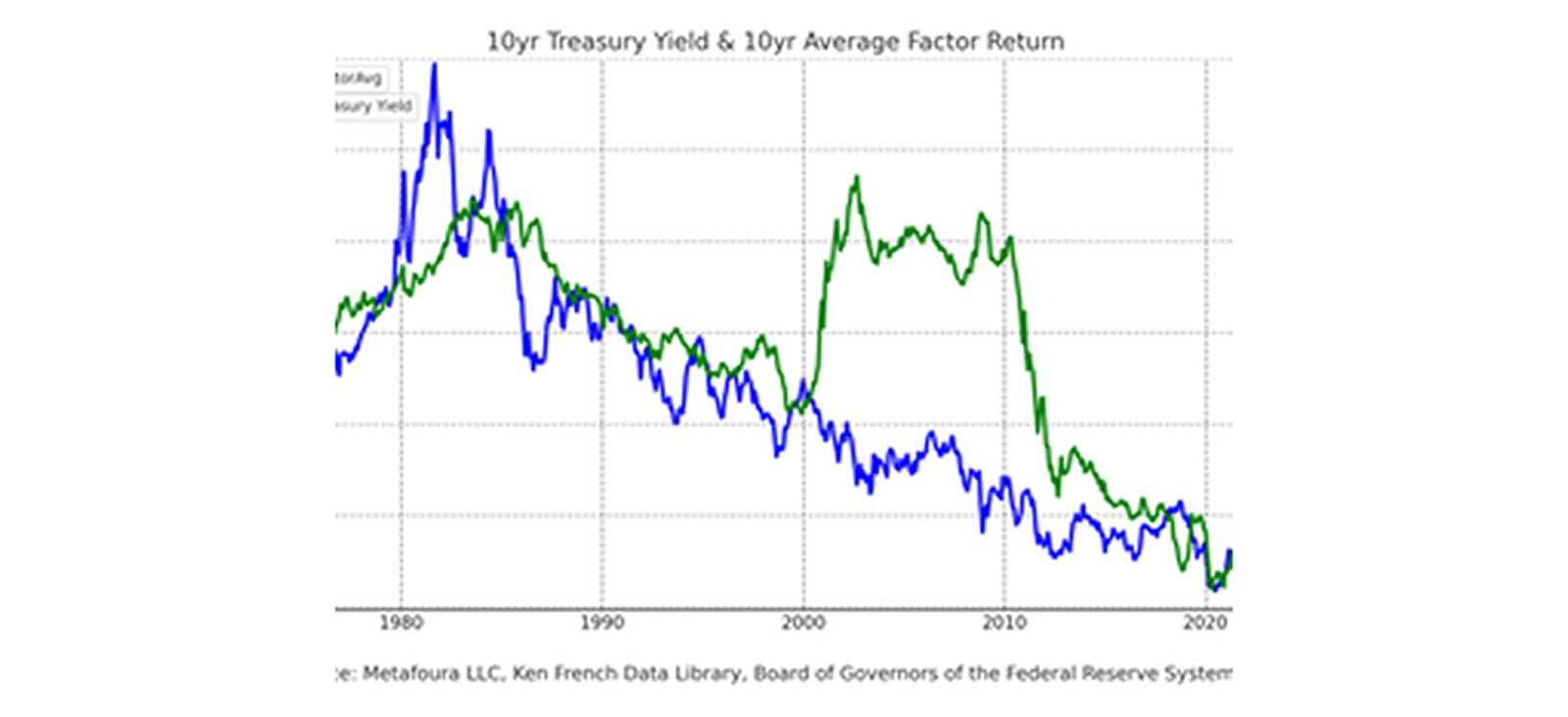

The Financial Times published my guest post, 'The quantitative climate change,' in which I highlight a half-century-plus connection between treasury yields and the performance of factor portfolios that quants need to succeed. The thirty-year-long treasury yield slide bottomed out in 2020, along with the end of the related three-year-long 'quant winter.' The long-term relevance of the treasury yield trend to factor portfolios important for quant performance is likely related to the Duration Factor introduced by Niels Joachim Gormsen and Eben Lazarus.

Take a look at 'The quantitative climate change’ in the Financial Times.

https://www.ft.com/content/6a38a189-70af-4c58-b24b-dbae36d8da8d