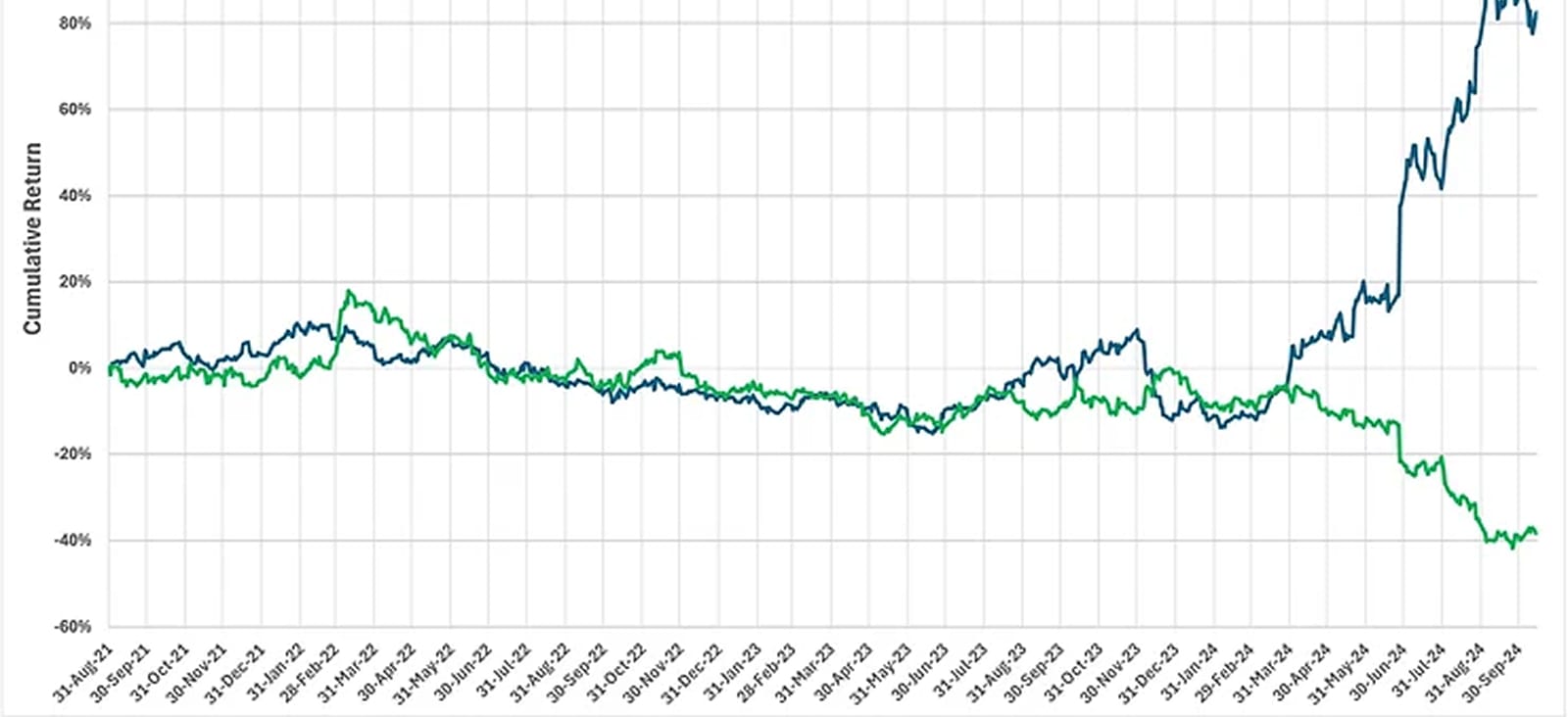

Two notable features of the 2024 market rally were the power of momentum and the dominance of large-cap stocks. The market peaked on July 16, but momentum and size peaked a week earlier, on July 9. The market now looks like it bottomed on August 5. That’s about a week after momentum and size bottomed on July 30.

The chart shows the S&P500, the momentum and size factor returns, and dashed line indicators for the top and bottom of these factor return trajectories. These factors are sector-neutral long-short monthly-rebalanced portfolios of stocks in the S&P500. The chart also includes the factor return for Free Cash Flow (FCF) yield, which bottomed on June 13 but started a sustained climb on July 5 – a few days ahead of the July 9 turning points for momentum and size. That climb peaked on August 5.

We would expect the FCF yield value factor to have the opposite risk profile from momentum and size. The path for FCF yield supports the observation that the momentum and size factors anticipated the recent market turning points. Or perhaps the factor moves helped produce these market turns. Monitoring these factors could provide a useful alert for what’s ahead.